2026/27 Budget Overview

This year the federal government has orchestrated four fundamental structural changes to Australia's taxation of private wealth, investment, and retirement savings. All four are contrary to previous assurances. For professionals, family businesses, investors, and retirees, the combined impact is substantial. There will be higher effective tax rates, significantly increased compliance costs, unavoidable restructuring costs, and years of legislative and administrative uncertainty.

The introduction of “Division 296” new additional taxes on superannuation earnings attributable to balances above $3 million and $10 million is now law and takes effect on 1 July 2026. The new 30% minimum tax on trusts, negative gearing restrictions, and capital gains tax changes announced in the 2026/27 Federal Budget are mostly up in the air at present. Some framework legislation for CGT and negative gearing policies was rushed through the lower house and has now been whitewashed via a senate “review”. There is a lot for taxpayers to consider and many unknowns.

Separately, the ATO has continued intensified compliance scrutiny across family trusts, companies and Division 7A, holiday houses, and SMSFs. Compliance expectations for ordinary family dealings have risen sharply, with Treasury and the ATO purposefully imposing, and then leveraging increased complexity to trap ordinary businesses and family groups with disproportionate penalties to raise additional revenue.

Whilst there is a desperate need for tax reform, recent policy changes are primarily revenue grabs. They have not been well thought through, and there has certainly been little real consultation on them. The number of apparently unanticipated problems identified with these measures is still growing. It is misleading to label this as “reform” because none of the underlying problems with the tax system are being addressed, especially its well documented overreliance on taxes on “income”. Continuing to tinker with outdated tax frameworks just translates into more complexity and inequity, neither of which Treasury has any concern about from within their protected bubble. Government continues to load up businesses and family groups up with complexity, compliance and risk though at the same time are perplexed by an ongoing decline in economic productivity.

The government’s broader ideological policy settings are gradually starving the economy of most key productive inputs. We are deprived of cheap and reliable energy, a productive workforce, and effective and simple taxes and regulations. Now, courtesy of the 2026/27 Budget, we are looking to be starved of aspiration, enterprise and investment. Economic productivity is at an all-time low, and headline economic growth is being held barely positive by unsustainable levels of immigration. The only savior could be artificial intelligence, though there are numerous risks with that and no coherent policy.

Please excuse this negativity but it must be expressed. As always, our aim is to provide understandable insight to assist you with practical solutions. If you have any queries or concerns, please contact us.

What's New

2026/27 Federal Budget – Increased Taxation and Complexity Under a False Narrative

30% Minimum Tax on Discretionary Trusts (Draft Legislation Expected Late 2026)

What it does:

From 1 July 2028, trustees of discretionary trusts will be required to pay a 30% minimum tax on the trust's taxable income. Beneficiaries will still include their distribution in their assessable income but will receive a non refundable tax credit for the trustee's 30% payment. Corporate beneficiaries will receive no credit, creating effective double taxation.

| Excluded trusts and entities | Excluded income and amounts |

|---|---|

| Fixed trusts and widely held unit trusts | Income from testamentary discretionary trusts (TDTs) STOP PRESS: Altered on 18/6/26 |

| Complying superannuation funds, including SMSFs | Primary production income |

| Special disability trusts | Income relating to “vulnerable minors” |

| Deceased estates, at least during administration | Amounts subject to non-resident withholding tax |

| “Fixed” testamentary trusts STOP PRESS: Altered on 18/6/26 – now supposedly includes TDTs |

STOP PRESS: New Announcement 18/6/26 - “Income from all types of testamentary trusts will be exempt from the minimum tax, including future discretionary testamentary trusts, with implementation details included in further consultation.” Warning: Treasury will continue its focus on restricting trust structures. Expect plenty of tricks, traps and complexity in the detail when it is eventually known.

Impacts of Trust Changes:

❌ Income splitting amongst low tax rate beneficiaries after 30th June 2028 will be Neutralised

❌ Tax effectiveness of post-budget testamentary discretionary trusts (TDTs) – Still be wary here!

❌ Corporate beneficiary distributions after 30th June 2028 result in total tax up to 69.71%

❌ Trust-to-trust loss planning likely neutralised because the 30% credit is non-refundable

❌ Trust distributions to charities will no longer be tax effective – Unforeseen issue. This may change

❌ Annual trust distribution planning becomes even more complex (if that is possible!)

❌ Compliance costs and risks for family groups will unavoidably increase on numerous fronts

❌ Trusts (other than TDTs) will remain viable only as a high-cost asset protection vehicle

❌ Costly restructuring may be the best option for some families and businesses

- Asset protection options will need to be reviewed – Binding Financial Agreements could assist

- Combined Budget measures will require review of most businesses and family groups

- Restructuring concessions (when known) may assist but many costs won’t be covered

! Low-income beneficiary distributions potentially waste the 30% tax non-refundable credits

! Company restructures can introduce Division 7A, franking credit, and payroll tax risks

! Earnings retained / re-invested in companies are arguably at high risk of franking policy changes

! Asset protection can easily compromise CGT Small Business Concessions in restructures

! Do not act prematurely on these measures - wait for legislation and proper detail

- Wages to family members may assist but watch “on costs”, administration, and ATO S 26.35 discretion

- Dividend Access Shares could provide distribution flexibility but there are tax policy risks!

- Superannuation is starting to look a whole lot better as a structure despite new Div 296 taxes

- Family investment companies may have merits - subject to high risk of imputation policy change

- TDTs in operation pre-Budget may be gold – STOP PRESS: await detail emerging from 18/6/26 backflip

Action:

- Check if TDT wills have an option to bypass any TDT if determined un-viable by executors at the time

- Start thinking about the impact of the Budget on your circumstances – don’t act yet

- Consider simplifying your financial affairs given Treasury’s attitudes to business and family groups

- Consider winding up trust structures where possible to avoid ever increasing risks they now attract

Key warning!!: Treasury and government are no longer able to disguise their contempt for hard working small business and family groups, and their inability to design and execute real tax reform. In the absence of proper reform, complexity is itself a tax with no benefit to the community. Because there is no real tax reform, there will be no respite for traditional business and family investment structures. Simplicity may be your only friend until there is real tax reform.

CGT & Negative Gearing Changes – Pulling Up the Ladder

What it does:

CGT discount replaced with CPI indexation + 30% minimum tax:

The current 50% CGT discount for assets held more than 12 months will be abolished for individuals, trusts, and partnerships for gains arising after 1 July 2027, including gains on Pre CGT assets. It will be replaced with:

- CPI indexation of the cost base (available after 12 months of ownership for tax residents only),

- This is combined with A 30% minimum tax on the net capital gain with some groups excepted*

- *Certain (unspecified at this point) recipients of means-tested government income support are exempt from the 30% minimum tax and will pay normal rates.

- New residential property (undefined) investors may elect to retain the 50% discount method instead of using the new CPI indexation + 30% minimum tax method.

CGT Grandfathering:

- Gains accruing before 1 July 2027 on post-CGT assets will continue to receive the 50% discount.

- A market valuation at 1 July 2027 or ATO apportionment formula (not yet devised) will be required to determine pre-reform and post-reform gains.

- Pre-CGT assets (acquired before 20 September 1985) will become partially taxable: gains accruing after 1 July 2027 will be subject to CGT

Other Carve Outs:

- Companies – they never had access to the 50% discount and also won’t have access to indexing.

- Superannuation funds – retain 1/3 discount after 12 months. Treasury was too scared to touch super again (for now) after the debacle around imposing new Div 296 taxes!

Update!! – 18 June 2026:

On 18/6/26 The Treasurer had a second attempt at the Budget and has announced some further carve outs for startups and innovation along with a slight change to the very complex CGT Small Business Concessions. For more – see below under “2026/27 Federal Budget – Version 2”.

Negative gearing restricted:

Deductions for losses on established residential properties acquired after 7:30 PM AEST on 12 May 2026 will be quarantined. Losses will be deductible only against:

- Rental income from residential properties, and or

- Capital gains from residential properties. Excess losses are carried forward indefinitely until death.

Exemptions from negative gearing quarantine:

- Residential properties acquired before 7:30 PM AEST on 12 May 2026 (including off-the-plan contracts exchanged but not yet settled).

- New residential properties (eligible “new builds” - undefined).

- Properties held in superannuation funds and widely held trusts.

- Certain build-to-rent and government-partnered housing developments.

Impacts of CGT and Negative Gearing Changes:

It is difficult to know where to start with all the implications. Many have been glossed over or not even on Treasury’s radar:

❌ Most scenarios with growth even moderately above inflation will result in a higher taxable gain

❌ Higher effective CGT rates for self-funded low-income taxpayers (due to minimum 30% tax rate)

❌ Timing of gains to take advantage of years with lower marginal rates is Neutralised

❌ Saving for first homes using growth assets or “rentvesting” will be much less viable unfortunately

❌ The complex and messy First Home Super Saver Scheme (FHSS) up to $50k may be a bit more compelling

❌ Non-residents get no indexing – CGT rules for non-residents have gradually gotten very nasty

❌ Valuations are required for most assets to optomise CGT up to 1 July 2027 – costly and unproductive

❌ Pre-20 Sep 1985(Pre CGT) assets are now subject to CGT after 1 July 2027 – quite unexpected

❌ Generally the tax system more broadly will provide little incentive for hard work, risk, and innovation

❌ Large increase in record keeping and calculation complexity – two histories for every asset and addition

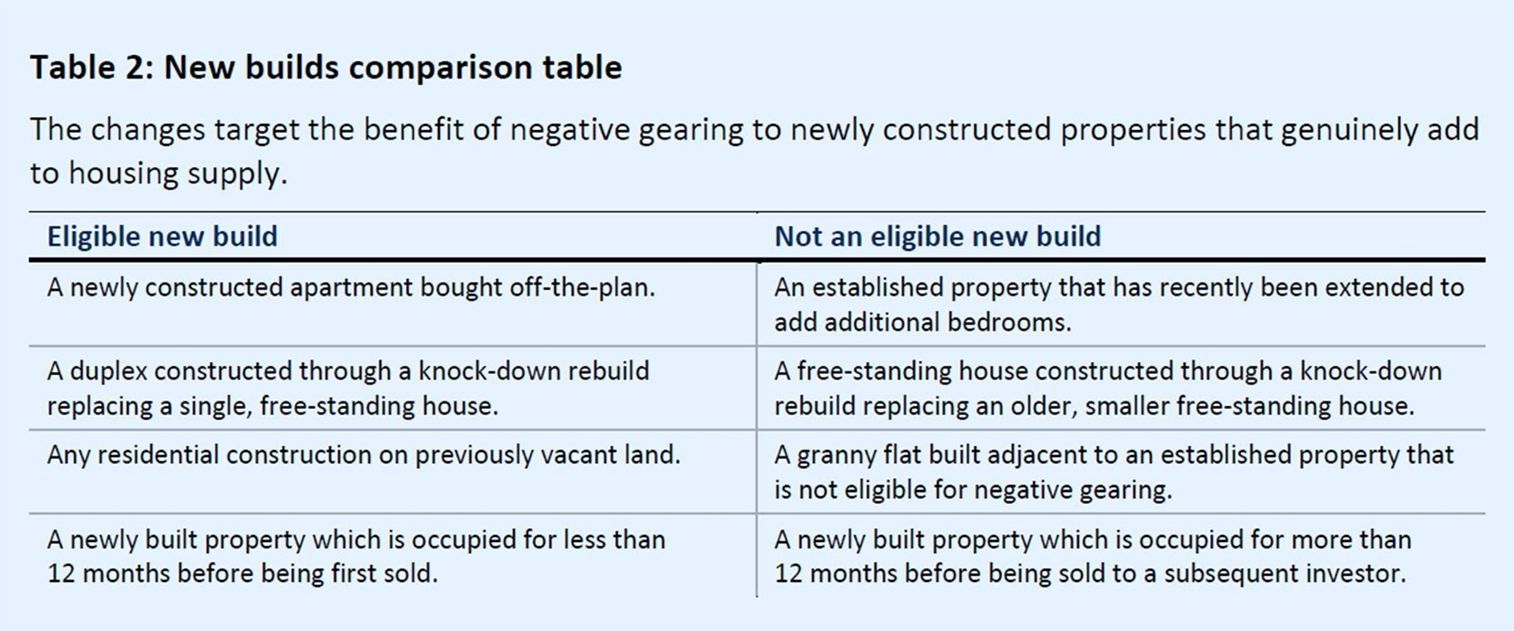

- It will be important to know how New Residential Property (”new build”) is to be defined - the following table from the Budget explainer shows likely inclusions in the final definition:

- The First Home Super Saver Scheme (FHSS) up to $50k might be worth revisiting

! There will be scope for disputes with ATO on valuations

! Keep state and local taxes in mind for various holding structures – especially Land Tax

Predictions:

- Budget measures may actually reduce supply of new residential dwellings

- With less supply and less incentive to invest in established property - rents will rise

- State governments will intervene to further regulate rents and increase tenants’ rights Increasing tenants’ rights will result in even less investment and less supply

- Young people’s access to the market will actually be reduced

- Young people will lose interest in saving via stock market investing due to high tax rates

- Existing residential property owners may “lock in” to preserve grandfathered tax status

- Recent first home buyers may experience negative equity

- Main residence is further elevated as preferred asset class – taxation of main residence will follow

- Bank of mum and dad flourishes - Increased reliance on intergenerational wealth transfers

- Residential property prices will fall overall due to reduction in after tax investment returns

- Potential investment bias away from residential housing and growth assets toward yield

- The combined Budget policies will trigger a recession. Most of it will eventually need to be dumped

Good Accountants will be hard to find: Accountants and tax agents are being loaded up with extraordinary levels of unpaid government work, complexity, compliance, and risk. At the same time their reputations are being tainted by the big four and incremental erosion of the Chartered Accountants (CAANZ) brand. There will be an exodus from the industry with no new blood attracted due to reputational shifts and false narratives about the impacts of AI.

Action:

- Start scoping for advice and market valuations – accountants and valuers will be thin on the ground

- Re-evaluate tax effectiveness of holding structures – Super likely now elevated in status

- Don’t shoot the messenger

2026/27 Federal Budget – Version 2 (Further versions to come!)

Update – 18 June 2026

⚠ Warning: Due to continuing community dissatisfaction with the Federal Budget handed down on 12th May, the Albanese Government announced changes on 18th July and will continue to announce further hastily devised policy changes to try and reduce political damage. The tax system is already an unsustainable mess, and these announcements will cause further uncertainty and complexity for taxpayers. Because they are politically motivated and without detail, it is certain that the final legislation and guidelines will be complex, restrictive and incorporate new traps for taxpayers. It is becoming very difficult for taxpayers and their advisers to know what to do in this terrible policy environment.

Following is a summary of the latest announcement as extracted from: Tax reform implementation for small business and startups Prime Minister of Australia

- Small business CGT relief broadened: The turnover threshold for the existing small business 50% active asset CGT reduction is proposed to increase from $2 million to $10 million, potentially extending eligibility to all 2.7 million active small businesses and 98% of active businesses. COMMENT: Note that three key branches of the complex Small Business CGT Concessions are excluded from the new threshold. Naturally that was glossed over in the press conference and sound bites.

- New innovative business concession: Treasury will release a consultation paper on a proposed Innovative

Business CGT Concession, intended to provide a 50% CGT discount to early-stage investors, founders and

employee share scheme participants in innovative start-up businesses. COMMENT: Ongoing uncertainty

and unnecessary complexity to patch up a poorly prepared and implemented Budget

- Testamentary trusts confirmed exempt: The Government has confirmed that income from all types of

testamentary trusts will be exempt from the proposed minimum tax, including future discretionary

testamentary trusts, with implementation details to be addressed through further consultation.

COMMENT: This is a complete backflip. Treasury has been caught out on its nasty intentions which remain.

Watch for sneaky “integrity” provisions and guidelines making testamentary trusts even more difficult to

operate

- More detail to be legislated: The Government has also confirmed that amendments will be made in the

Senate rather than left to legislative instruments, which should provide greater certainty on key

implementation details. COMMENT: Caught again! The government has backed down on the extent of

ministerial discretion given to the Treasurer to make up these rules as he goes. “Now that’s a good thing!”

FINAL COMMENT:

The initially stated objectives of the Budget were reasonable and adjustment of housing

settings necessary. This could have been easily done by tinkering with the levels of CGT Discount. There could

even be different discount percentages depending on period of ownership or asset type. That would have been

so simple. Instead, we get a complex mess which without doubt will have to be unwound, with the unwinding

creating even more disruption. We are well on the road to recession with policies like these.

Other Budget Measures

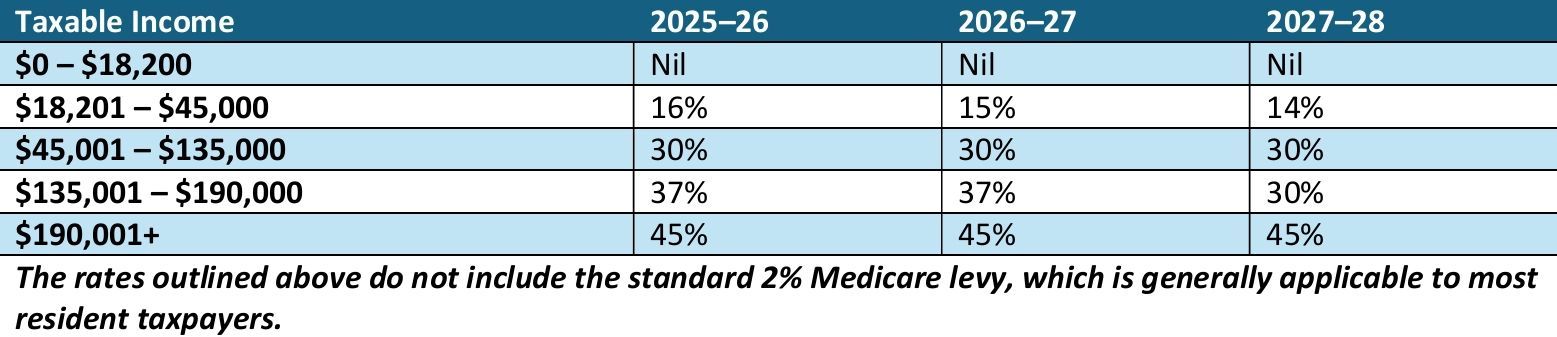

Individual Tax Rates (2026–27 to 2027–28)

New Working Australians Tax Offset ($250) – From 2028 Income Year

This is an un-indexed non-refundable tax offset that will apply automa cally through the tax system. It reduces tax

payable solely on income earned from work (wages, salary, or sole-trader income).

Impact:

A very modest handout considering ongoing impacts of inflation on and bracket creep – at least it’s not complex!

$1,000 Standard Deduction for Work-Related Expenses – From 2026-27

This was combined with the CGT and Negative Gearing changes so they could be rushed through. The bill is not yet

law but is likely to pass. Resident taxpayers deriving assessable labour (Labor?) income can claim up to $1000 against

that income. Apparently, this amount can be optionally claimed regardless of the actual level of expenses incurred!

Excluded from the deduction on are Sole Traders, Independent Contractors, individuals engaged under labour hire, and

individuals with Personal Services Income. Where work expenses are above $1000 taxpayers have the op on of

claiming under normal substantiation requirements.

Impact:

- The appearance of free money in the form of an increased refund – a handy vote buyer

- Will kill off some nuisance record keeping for many workers

- This change has a sneaky lesser known FBT increase attached which is very anti small business (see below)

- For many professionals and tradespeople, actual expenses will exceed $1,000 so no benefit

⚠WARNING: FBT "Otherwise Deductible" and Work Items Exemptions Removed

Buried in the draft legislation on for the $1,000 standard deduction is a potentially very nasty sting for small businesses

and their employees. This has been spun as necessary to prevent double dipping on expenses covered by the $1000

standard deduction. In reality, it has a far greater impact on taxpayers who would not normally benefit from the

$1000 concession. COMMENT: This lesser known change applies to reimbursements, employer-paid expenses, and

salary-packaged expenses. It will prove to be very costly and disruptive to small businesses and their employees.

Current treatment: If an employer provides or reimburses a work-related expense (e.g. work related travel or self

education expenses), and the employee would have been entitled to claim a tax deduction if they had paid for it

themselves, the employer can apply the “otherwise deductible rule” to reduce the taxable value of the benefit—

often to zero—so no FBT is payable. It is convenient and can be advantageous if GST credits are available. Also,

certain work-related items (such as laptops, phones and tools of trade) given to employees may be fully exempt

from FBT under a specific exemption on where they are primarily used for work purposes. The employer can also claim

GST on these items where applicable where the employee cannot. Certain expenses excluded from being covered

by the standard deduction on included income protection, personal sickness and accident insurance premiums, along

with payments for membership of a union or other trade, business or professional association.

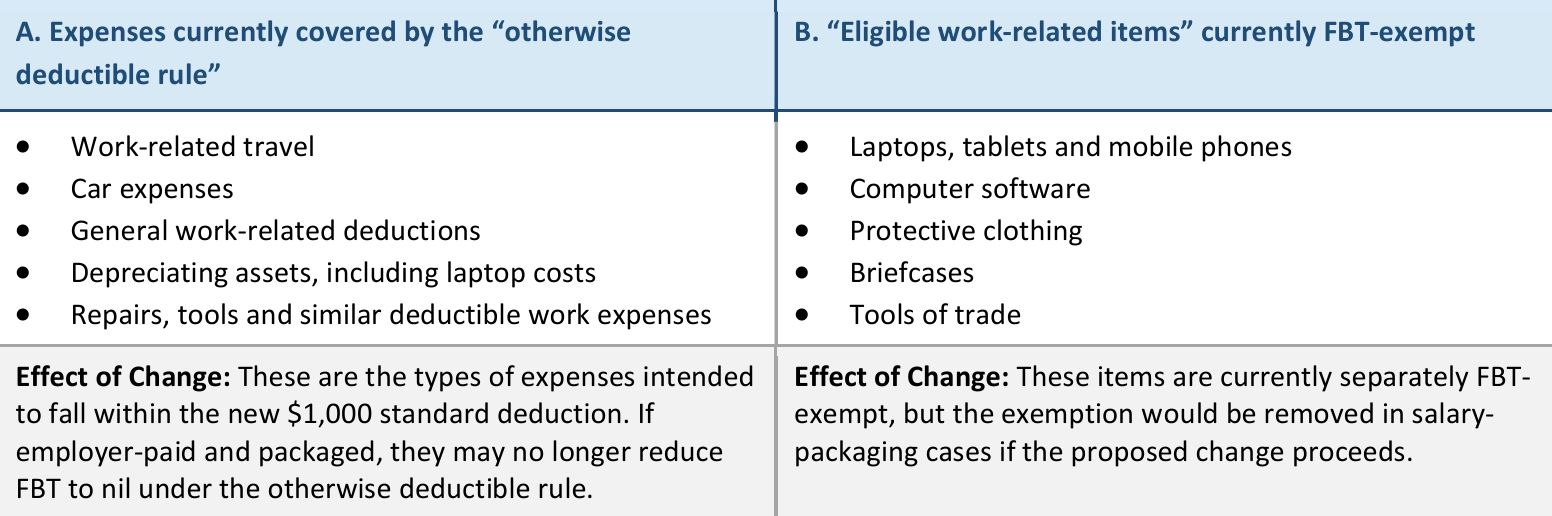

New treatment: WARNING – Salary Packaging FBT Trap: Under the proposed rules, both The “otherwise

deductible rule” and The FBT exemption on for work-related items (e.g. laptops, phones, tools of trade) are effectively

removed for salary packaged benefits:

These are the categories:

WARNING: The potential impact of these very anti-business changes is:

! The employer faces an FBT Liability on the grossed GST inclusive up value at a rate of 47%

! Salary Packages and employee related expenses will have to be renegotiated.

- While the proposed rules significantly impact salary packaged benefits, there remains scope for employers to fund work-related costs directly. The key distinction is that the expense must be employer-driven and not provided in exchange for reduced salary—otherwise it risks being treated as salary packaging and subject to FBT.

This has created a big mess for businesses to sort out.

Private Health Insurance Rebate: Age-Based Uplift Removed

From 1 April 2027, the Government will phase out the age-based uplift of the Private Health Insurance (PHI) rebate

for Australians aged 65 and over.

Removing the age-based uplift cuts the PHI rebate for over-65s by 4–8 percentage points, increasing premiums

by hundreds to over $1,000 per year for many—shifting a significant share of health insurance costs onto retirees.

FBT Concession for Electric Cars: Chris Bowen’s Net Zero Gravy Train Slows Down

The generous 100% FBT exempt on for certain electric vehicles will be phased out from 1 April 2027.

Current concession (un l 31 March 2027):

- 100% FBT exemption on for eligible EVs (battery electric, hydrogen fuel cell, PHEVs)

- Applies where the vehicle price is below the luxury car tax threshold ($91,000 for 2026)

New rules (from 1 April 2027 – for new / changed arrangements):

- EVs under $75,000 → 25% FBT discount (FBT on 75% of value)

- $75,000 to luxury car threshold → Full FBT (no exemption)

- Above threshold → Full FBT

Final phase (from 1 April 2029):

• All EVs: 25% FBT discount, regardless of price (capped at luxury car threshold)

- This has been a very generous concession. The planning opportunity here is packaging eligible vehicles before 1 April 2027

- For higher-value EVs above the luxury car tax threshold, the period from 1 April 2027 to 31 March 2029 is the least favourable, with full FBT applying.

- From 1 April 2029, a partial concession returns (25% discount), but this is still materially less generous than the current full exemption available for qualifying vehicles entered into before April 2027.

SMALL BUSINESS MEASURES IN THE BUDGET – MORE POLITICAL THEATRE!

$20,000 Instant Asset Write-Off – Permanently Extended (for now)

Small businesses with turnover under $10 million can immediately deduct assets cos ng less than $20,000 (GST

exclusive, per asset). This applies for the 2026 Financial Year but will now be made permanent.

- Instant asset write offs are used as a political tool without any genuine regard for small business

- Many people don’t realise that it is simply a tax deferral similar to accelerated depreciation on claims

- These write offs can reverse nastily when the asset is sold – Covid limits up to $150k have caused later problems

- Always worth taking advantage of especially around year end. For details: Instant asset write-off ATO

Company Loss Carry-Back Reintroduced – There Are Important Limitations

For tax years commencing on or a er 1 July 2026, companies will be able to carry back a tax loss and offset it against

tax paid up to two years earlier.

Note: The refundable amount is capped by prior tax paid and the company’s franking account balance – meaning

businesses that have not retained profits or tax paid (franking balance) in prior years will receive li le or no benefit.

- This will be relatively automatic to claim where available from the 2027 tax year onward

COMMENT ON BUSINESS MEASURES:

The small business sector makes up of 97% of all businesses, employs millions of Australians and contributes around one-third of GDP. These businesses are built by proprietors who take real financial risks, work long hours, and shoulder a disproportionate share of administrative and compliance obligations — often effectively acting as unpaid intermediaries for government systems and employee obligations. Proprietors of these businesses work hard, take many risks, and do a lot of administration work for the government and their employees for free. The policy approach toward them is patronising to say the least. What we get are carefully designed, tightly constrained measures that create positive headlines but deliver limited, and sometimes illusory, practical benefit for a large portion of the sector.

“Claytons” Loss Refundability for Small Startups

For tax years commencing on or after 1 July 2028, start-up companies with aggregated annual turnover of less than

$10 million that generate a tax loss in their first two years of opera on will be able to utilise the loss to generate a

refundable tax offset.

Important limitation: The offset will be limited to the value of fringe benefits tax and withholding tax on wages paid

in respect of Australian employees in the loss year.

- This smells of creating the appearance of doing something (especially given the deferred start date)

- Real startups rarely pay founders wages or fringe benefits in early years so this is fake

Research and Development (R&D) Tax Incentives Adjusted from 1 July 2028

The Government is reshaping the R&D tax incentive from 1 July 2028, with the aim of making it more generous for

genuine “core” R&D activities, while enlightening rules around what qualifies.

- For businesses involved in problem-solving, experimenta on, or developing something new (products, processes, so ware, systems), R&D Incen ves should be kept on the radar.

COMMENT ON BUSINESS MEASURES: The small business sector makes up of 97% of all businesses, employs

millions of Australians and contributes around one-third of GDP. These businesses are built by proprietors who

take real financial risks, work long hours, and shoulder a disproportionate share of administrative and compliance

obligations — often effectively acting as unpaid intermediaries for government systems and employee

obligations. Proprietors of these businesses work hard, take many risks, and do a lot of administration work for

the government and their employees for free. The policy approach toward them is patronising to say the least.

What we get are carefully designed, tightly constrained measures that create positive headlines but deliver

limited, and sometimes illusory, practical benefit for a large portion of the sector.

Disclaimers

Financial Product Advice

Nothing in this advice is intended as ‘financial product advice’ as defined by the Corporations Act (as amended by the Financial

Services Reform Act 2001). We are not licensed to provide ‘financial product advice’ which includes recommendations regarding

contribution to or withdrawal from, or specific investments within a particular superannuation fund (including a Self-Managed

Superannuation Fund). You should consider if it is in your interests seeking advice from an Australian Financial Services Licensee

before making decisions in relation to a financial product.

Currency of Income Tax Advice

Any taxation advice included in this correspondence is current to the date of writing. Taxation laws in Australia are complex

and constantly changing. The government often changes rules effective from the date announced and, in some cases,

retrospectively. If there is any delay in the use of this advice you should consider having it refreshed.

Quality of information

Before relying on the information on this newsletter, users should carefully evaluate its accuracy, currency, completeness, and

relevance for their purposes, and should obtain professional advice relevant to their particular circumstances. We and

associated parties cannot guarantee nor assume any legal liability or responsibility for the accuracy, currency or completeness

of the information or material.

Links to external websites

This newsletter may contain links to other websites which are external to our newsletter and website. It is the responsibility of

the user to make their own decisions about the accuracy, currency, reliability, and correctness of information contained in linked

external websites.

Linkage to external websites should not be taken to be an endorsement or a recommendation of any third-party products or

services offered by virtue of any information, material or content linked from or to this website. Users of links provided by this

website are responsible for being aware of which organisation is represented or providing the information or material on the

website they visit.

Views or recommendations provided in linked websites do not necessarily reflect our views or recommendations, nor the views

or recommendations of associated parties.

Security of our website

Users of our website should be aware that the World Wide Web is an insecure public network that gives rise to a potential risk

that a user's transactions are being viewed, intercepted, or modified by third parties or that files which the user downloads may

contain computer viruses or other defects.

We and associated parties accept no liability for any interference with or damage to a user's computer system, software or data

occurring in connection with this website. Users are encouraged to take appropriate and adequate precautions to ensure that

whatever is selected from this website is free of viruses or other contamination that may interfere with or damage the user's

computer system, software, or data.

Liability limitation

Liability limited by a scheme approved under Professional Standards Legislation. Confidentiality Notice: The contents of this e

mail and any attachments are confidential. It must not be used, distributed, copied or read by any person other than the

addressee. If this transmission has been received by any person other than the addressee please return to us

immediately. Unauthorised use, disclosure, copying or reliance on the contents or attachments of this e-mail by anyone

other than the named addressee may be unlawful