From 1 July 2026, an extra tax applies to super balances above $3 million. Here is what it means in plain English, when it pays to act, and where the traps lie — including how the 2026/27 Federal Budget changes the case for leaving super behind.

1. The Basics in 60 Seconds

- Brand new tax: Division 296 is a separate, additional tax that sits on top of all existing fund-level and personal taxes. It is assessed to the member personally, not the super fund (although you can elect to have it paid from your super via a release authority).

- Start date: 1 July 2026. The first measurement point is 30 June 2027 and the first assessments will be issued by the ATO – likely sometime in 2028 for SMSF members.

- Two thresholds (indexed): the Large Super Balance Threshold (LSBT) of $3 million and the Very Large Super Balance Threshold (VLSBT) of $10 million. Both index to CPI in jumps of $150,000 and$500,000 respectively.

- The formula:

15% × (proportion of TSB over $3m) × earnings

+

10% × (proportion of TSB over $10m) × earnings

- "Earnings" means: your share of the fund's realised investment income (dividends, interest, rent, trust distributions, franking credits) plus realised capital gains (after the 1/3 super CGT discount), less tax-deductible expenses. GOOD NEWS: unrealised gains are NOT taxed – the controversial original proposal was dropped before the law passed.

- Transitional rule for 2026/27 only: the proportion is based on your TSB at 30 June 2027 only. So withdrawing super before 30 June 2027 (if you are eligible) can reduce or eliminate the first year's bill.

WARNING: from 2027/28 onwards the calculation uses the HIGHER of your opening or closing balance – large mid-year withdrawals will no longer save you.

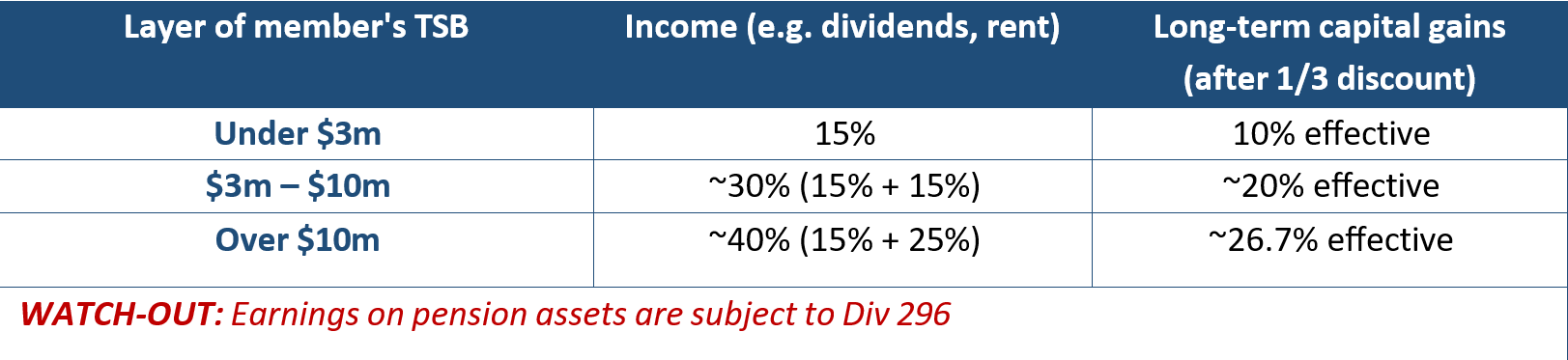

2. What Does It Do to Total Tax on Fund Income & Gains?

The table below shows the total effective tax rate (fund tax + Div 296) on each layer of a member's balance, on realised investment income and on realised long-term capital gains (after the 1/3 super CGT discount).

3. How Does It Compare to Personal Marginal Rates and Other Structures?

The comparison below shows where each common structure sits today and where it will sit from 1 July 2028 once the 2026/27 Federal Budget's proposed 30% minimum tax on discretionary trusts takes effect.

| Structure | First Name | Last Name | Email Address |

|---|---|---|---|

| Top Personal Marginal Rate | 47% Incl. Medicare | Marginal rates reducing (Stage 3+ cuts from 1/7/26 & 1/7/27) | Stable; only structure to fall in rate |

| Low-Income Spouse/Retiree | 0%-37% | 0% – 37% | Newly attractive given trust changes |

| Family Discretionary Trust | Streamed at Beneficiaries' rates (16%-47%) | 30% MINIMUM at trustee level — credits non-refundable | Income-splitting benefit largely gone from 2028 |

| Bucket/Corporate Benefiiciary | 25%/30% | ~69.7% on NEW trust distributions (no credit refund) | Commercially dead as a new bucket from 2028 |

| Standalone Investment Company | 25%/30% | 25% / 30% (unchanged) | Surviving alternative - but Div 7a, not CGT discount, franking risk |

| Fixed/Unit Trust | Marginal rates of unit Holders | Excluded from 30% minimum – taxed at unit holders' rates | Weak asset protection; fixed-trust definition still being finalised |

| Super - Under $3M (accum) | 15% / 10% effective CGT | 15% / 10% (unchanged) | 0% pension phase intact |

| Super $3m to $10m | 15% / 10% effective CGT | ~30% income / ~20% CGT (incl. 15% Div 296) | Pension exemption added back for Div 296 TSB resets on death - Useful estate planning lever |

| Super Over $10M | 15% / 10% effective CGT | ~40% / ~26.7% (incl. | Pension exemption added back for Div 296 TSB resets on death - Useful estate planning lever |

Note: This table needs to be considered in conjunction with other changes announced in the Budget and to tax settings outside od super mor generally.

What this comparison really tells us

- BIG SHIFT: The 2026/27 Budget's proposed 30% minimum tax on discretionary trusts from 1 July 2028 closes off the historical "withdraw from super and stream via a family trust + bucket company" alternative for most clients.

- TIP: Super inside Div 296 territory (30% – 40%) is, paradoxically, more competitive after the Budget than it was before — because the main alternative (trust + bucket company) has moved from 25% – 37% effective to a 30% minimum (or ~69.7% if a corporate beneficiary is still used).

- WATCH-OUT: The clear winners from the Budget package are (a) personal ownership in a low-income spouse's name, (b) standalone investment companies, and (c) super up to $3m. Fixed/unit trusts remain available but the protective benefit is weak and the fixed-trust definition is still being finalised.

WARNING: Franking policy risk is elevated. Successive governments have flagged interest in limiting franking credit refundability. Don't build a structure that only works if franking refunds continue indefinitely.

4. Should I Increase or Reduce My Super Balance?

Scenario-based pointers

- Below $3m today: Generally KEEP CONTRIBUTING. Super at 15% / 10% effective is still the most tax-effective wrapper available. Maximise concessional carry-forward (if TSB under $500,000) and NCC bring-forward (if TSB under $1.76m at 30 June 2025) before your balance grows close to $3m.

- Approaching $3m: Be deliberate. A small breach of $3m only attracts Div 296 on a small proportion of earnings, so it is rarely a reason to stop contributing entirely. TIP: consider splitting contributions to a lower-balance spouse to keep both balances under $3m.

- Between $3m and $5m: Review annually. In most cases staying in super still wins – especially if you are in pension phase with strong franking credit refunds. Model with realistic asset turnover (low turnover = low realised earnings = low Div 296).

- Between $5m and $10m: Genuine alternatives start to make sense — but post-Budget, the realistic options are a low-income spouse's personal name or a standalone investment company, not a family trust + bucket company. Model after-tax 10–15 year returns including the one-off exit cost.

- Over $10m: Strong case to consider partial withdrawals if eligible (typically age 60+ and condition of release met). The 25% Div 296 layer above $10m bites quickly. The destination is most likely an investment company or low-bracket spouse — see Section 6.

WARNING: don't let the Div 296 tail wag the dog. The cost of EXITING super — fund CGT on disposal or in-specie transfer, plus stamp duty on property, plus transaction costs — is often a much bigger one-off hit than several years of Div 296. Model both before deciding.

5. Is It Worth Withdrawing and Investing Elsewhere?

The honest answer: sometimes – but rarely as obvious as it first appears.

The decision depends on five variables that interact:

- Ongoing tax differential: Div 296 effective rate (30% or 40%) vs the alternative entity's post-2028 rate (e.g. 25% / 30% investment company; marginal rates in a low-bracket spouse's name; not a discretionary trust at the new 30% minimum).

- One-off exit cost: The fund realises CGT on every asset sold or transferred out. If your SMSF holds property bought 15 years ago, this can be a very large tax event – often dwarfing 5–10 years of Div 296 tax.

- Loss of pension-phase exemption: Future earnings inside a pension up to the Transfer Balance Cap are exempt from fund tax (though not from Div 296). Once you withdraw, that exemption is gone forever.

- Time horizon: Younger members have more years for Div 296 to accumulate; older members closer to estate-planning events may prefer to stay in and use the death-time TSB reset (see Section 7).

- Fund liquidity: SMSFs with lumpy illiquid assets (commercial property, private company shares, unlisted units) may struggle to fund a Div 296 release authority. STRATEGY: model liquidity NOW so you are not forced to sell at the wrong time later.

- Don’t forget Death Benefits Tax: Where benefits are ultimately paid to non dependants for tax purposes (e.g. adult children), the taxable component is generally subject to 15% + Medicare levy (effectively 17%). STRATEGY: Integrate estate-planning timing into the Div 296 decision—not after it

6. The 2026/27 Federal Budget – What it Means for the "Take it Out of Super" Decision

The 2026/27 Federal Budget's biggest impact on the Div 296 decision is not what it did to super – it's what it did to the alternatives. Three changes materially affect whether withdrawing from super and re-investing elsewhere makes sense.

a) 30% minimum tax on discretionary trusts from 1 July 2028

The trust + bucket company model that has historically been the go-to alternative to super has effectively been neutered. Super at 30% – 40% effective may now be the BETTER answer.

b) Personal tax cuts from 1 July 2026 and 1 July 2027

Personal marginal rates are falling slightly; the top bracket remains at 47% but middle brackets reduce. This very modestly improves the case for holding investments in a low-income spouse's name — particularly a retired or part-working spouse. TIP: Equalising super between spouses (contribution splitting, re-contribution strategies) remains the single most powerful pre-30 June lever for managing combined Div 296 exposure.

c) Other Budget items that interact

CGT discount and negative gearing changes will generally increase the tax on investments held outside of super.

WARNING: Any decision to wind down super and rebuild outside should NOT be made until the trust tax legislation is enacted (expected late 2026) and the rollover relief window detail is published. Premature restructuring is the bigger risk than waiting.

Putting it together – should you still consider exiting super?

The Budget has reshuffled the deck enough that pre-Budget advice on this question is now usually wrong. The post-Budget rules of thumb:

- Under $3m: Keep contributing. The story hasn't changed for you.

- $3m – $5m: In most cases, STAY. The post-Budget alternatives are now also taxed at around 30% (or higher) and lack super's pension-phase exemption on the first $3m.

- $5m – $10m: Situational. The realistic alternatives are a low-income spouse's personal name or a standalone investment company. The 30%-minimum trust is rarely the answer post-2028.

- Above $10m: There is still a real case for partial withdrawal, but the alternative is now most likely a standalone investment company (25% / 30% on income, no CGT discount) or holdings in a low-income spouse's name. Model with the 2027/28 alternative tax rules in mind, not today's.

IMPORTANT: A decision that looked obvious 12 months ago “pull it out and use a family trust" — is now usually wrong. Don't act on pre-Budget advice without re-running the numbers.

1. Estate Administration – A Significant New Problem

Division 296 introduces some difficult issues for executors and surviving spouses that have not previously existed in relation to their super.

- Death resets TSB to nil – but only going forward: From the year AFTER death there is no further Div 296 liability on the deceased. BUT the deceased's estate will still receive a Div 296 assessment for the YEAR OF DEATH if their opening TSB was Example: A member dies in June with $5m in super. Earlier in the year the SMSF sold a property crystallising a $1m capital gain. The estate gets a Div 296 bill calculated on the proportion of those earnings above $3m – potentially well over $100,000 – even though the member is no longer alive.

- Reversionary and death benefit pensions to a spouse: Inherited super instantly adds to the surviving spouse's TSB (no 12-month grace like the Transfer Balance Cap rules). A spouse with $2.5m of their own super who inherits $3m may immediately be pushed into Div 296 territory for the rest of their life.

WATCH-OUT: If a death is anticipated, the timing of asset sales inside the fund matters. Realising a large capital gain in the year of death can create a Div 296 liability that wouldn't exist if the sale were deferred. Conversely, sales after 30 June following death attract no Div 296 (deceased's TSB is nil).

STRATEGY: Re-contribution strategies, BDBNs and reversionary pension nominations all need a refresh – especially where the surviving spouse already has substantial super in their own right. Splitting benefits to adult children (where eligible) may be more tax-effective than reversion to spouse.

- Insurance proceeds into super: If life insurance is paid into the fund on death and retained in pension phase by the spouse, it increases the spouse's TSB and Div 296 exposure. Consider whether some or all should be paid out as a lump sum to the estate instead.

WARNING – cashflow timing: LPRs may receive a Div 296 assessment 12–18 months after year end (SMSFs lodge late). If the death benefit has already been paid out, the executor may have no super left to pay the bill from. The liability falls on the estate. Hold back sufficient cash until the Div 296 position for the year of death is finalised.

Next Steps – What to Do Before 30 June 2027

1. Get an accurate TSB picture by 30 June 2026 (and refresh annually). Identify any members likely to exceed $3m at 30 June 2027.

2. Refresh SMSF asset valuations with supportable evidence – this is now critical, not just good practice.

3. Consider the SMSF cost-base reset election for pre-1 July 2026 assets (an irrevocable, all-or-nothing decision made before the 2026/27 annual return is due).

4. Model fund liquidity for a Div 296 release authority – particularly for SMSFs holding property or unlisted assets.

5. Review estate planning documents – BDBNs, reversionary nominations, insurance ownership, and surviving-spouse TSB exposure.

6. Wait for the trust tax legislation before committing to any wind-down of super – the alternative-structure rules are still being finalised.

7. Talk to us BEFORE acting on any lump-sum withdrawal or restructure. The numbers genuinely need to be modelled.

Disclaimers

Financial Product Advice

Nothing in this advice is intended as ‘financial product advice’ as defined by the Corporations Act (as amended by the Financial Services Reform Act 2001). We are not licensed to provide ‘financial product advice’ which includes recommendations regarding contribution to or withdrawal from, or specific investments within a particular superannuation fund (including a Self-Managed Superannuation Fund). You should consider if it is in your interests seeking advice from an Australian Financial Services Licensee before making decisions in relation to a financial product.

Currency of Income Tax Advice

Any taxation advice included in this correspondence is current to the date of writing. Taxation laws in Australia are complex and constantly changing. The government often changes rules effective from the date announced and, in some cases, retrospectively. If there is any delay in the use of this advice you should consider having it refreshed.

Quality of information

Before relying on the information on this newsletter, users should carefully evaluate its accuracy, currency, completeness, and relevance for their purposes, and should obtain professional advice relevant to their particular circumstances. We and associated parties cannot guarantee nor assume any legal liability or responsibility for the accuracy, currency or completeness of the information or material.

Links to external websites

This newsletter may contain links to other websites which are external to our newsletter and website. It is the responsibility of the user to make their own decisions about the accuracy, currency, reliability, and correctness of information contained in linked external websites.

Linkage to external websites should not be taken to be an endorsement or a recommendation of any third-party products or services offered by virtue of any information, material or content linked from or to this website. Users of links provided by this website are responsible for being aware of which organisation is represented or providing the information or material on the website they visit.

Views or recommendations provided in linked websites do not necessarily reflect our views or recommendations, nor the views or recommendations of associated parties.

Security of our website

Users of our website should be aware that the World Wide Web is an insecure public network that gives rise to a potential risk that a user's transactions are being viewed, intercepted, or modified by third parties or that files which the user downloads may contain computer viruses or other defects.

We and associated parties accept no liability for any interference with or damage to a user's computer system, software or data occurring in connection with this website. Users are encouraged to take appropriate and adequate precautions to ensure that whatever is selected from this website is free of viruses or other contamination that may interfere with or damage the user's computer system, software, or data.

Liability limitation

Liability limited by a scheme approved under Professional Standards Legislation. Confidentiality Notice: The contents of this e-mail and any attachments are confidential. It must not be used, distributed, copied or read by any person other than the addressee. If this transmission has been received by any person other than the addressee please return to us immediately. Unauthorised

use, disclosure, copying or reliance on the contents or attachments of this e-mail by anyone other than the named addressee may be unlawful